Every year tech & durables manufacturers invest billions of dollars in trade spending – funding activities such as price promotions, in-store displays, merchandising support, and other incentives designed to encourage retailers and distributors to stock and promote the brand’s products. However, this spend is not always leveraged to best effect. Rather than balancing spend across activities that increase promotion performance to drive sales volume and value and incremental profit, the focus is too often on merely defending market share through pricing.

But there’s hope! Using gfknewron Predict, which draws on the global reach of our world-leading Tech & Durables retail panels, we have identified brands who have escaped the price race to the bottom and analyzed the strategies they are employing to succeed. This is what we learned:

Brand strength and above-average promotion performance go hand-in-hand

Our analysis of brands across 7 countries and 4 product categories shows empirically that the secret to winning the promotional game lies in the strength of your brand.

Strong brands create a pull that enhances the performance of their promotional activity, resulting in a revenue uplift which is, on average, 3% higher than the market overall. This above-average promotional performance of strong brands was visible in 20 of the 28 ‘cells’ assessed (where a cell refers to a specific category in a specific country).

Our 3-step analysis

As a first step, we analyzed the concentration of each category within each market. This supported the interpretation of results later on, ensuring that the promotion performance measurements were the result of differences in brand strength rather than market characteristics.

To measure the market concentration, we used the Herfindahl-Hirschman Index (HHI). This index measures the concentration of different brands’ market shares within a category and is an indicator of the amount of competition within that category. Ranging from 0 to 1.0, a lower value indicates a less concentrated landscape (a high number of smaller brands, allowing for lots of competition), while a higher value indicates a more concentrated landscape (a small number of larger brands controlling the scene).

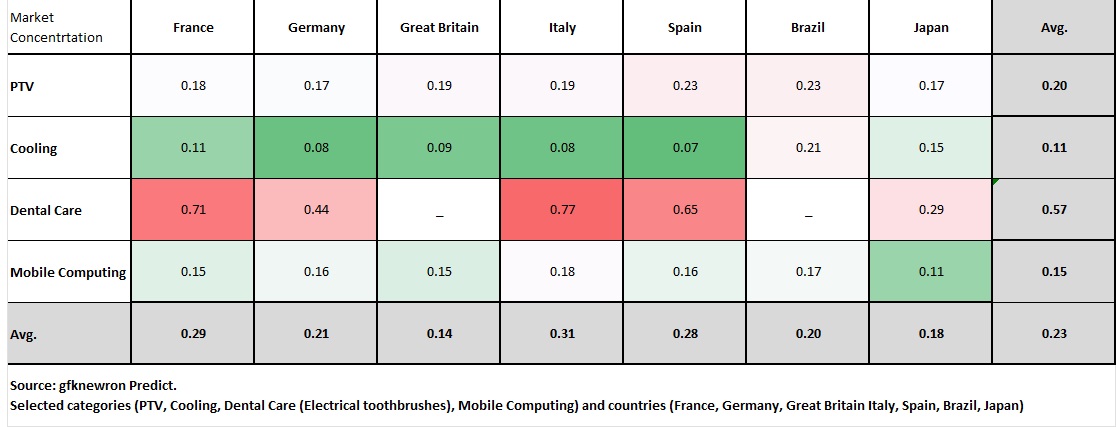

Table 1: Concentration of markets

Table 1 shows the concentration of each market. Dental Care is a highly concentrated category in each market with an HHI between 0.29 and 0.77 indicating that a couple of brands are dominating. On the other extreme, Cooling is a highly fragmented category in each market with a lot of players competing for share.

We then identified the ‘power’ brands within the market – those able to create a pull-through of their brand equity. ‘Power’ brands were taken to be those with a market share (revenue) of at least 0.5% and proportionally more market share in the premium-end. This meant that not only large brands were included in the power rating, but also smaller brands running a successful premiumization strategy.

As the final step, we compared the promotion performance of the power brands against that of the market average. Here, we analyzed the promotion revenue uplift that the brands within each market generated over 52 weeks (week 45 2022 to week 44 2023) and set it in relation to the total revenue generated during promotions. A high percentage achieved at this stage of the analysis indicates that the brand was able to drive incremental revenues during their promotional activity.

Conclusion – impact of ‘power’ brands on promotion performance

In 20 out of the 28 cells (a category within a country) we see a higher promotional uplift generated by power brands compared to the market average – especially within the categories of Cooling and Dental Care.

However, there is important variation. Brand strength seems to make a huge difference in promotional uplift for a category in some countries, while making next to no difference in other countries, or even returning a negative effect.

Mobile Computing: power brands in Japan and Italy show a clear advantage in the effectiveness of their promotional activities – coming in respectively at +24 percentage points (pp) and +7pp above the average performance. But in Spain and Brazil the power mobile computing brands perform worse in their promotional activity, coming in at -3pp below the average.

PTV: for this category, it is Germany (+6pp) and France (+3pp) where power brands perform most strongly in their promotional activity, while those in Brazil perform below the average (-3pp).

Cooling: power brands in Brazil (+9pp), France and Germany (both +8pp) are strongly ahead, while those in Spain (+1pp) are level with the average.

Dental Care (electric toothbrushes): the picture for this category is much more even across all countries analyzed, with the highest difference being in Germany, where power brands rated +2pp higher than the average.

The key take-away for power brands lies in approaching the market differently than the mass, yet taking market characteristics (market drivers) into account.

“Marketing spend needs to be focused on activities where they will achieve the greatest net effect short and long-term – not only considering instant sales performance but also taking long-term investments into brand value into account. This requires a genuinely holistic grasp of the landscape that incorporates the market trends, the needs and wants of consumers, and an in-depth understanding of trade partners and competitors. This is where GfK can help with a combined offering of market and consumer insights enriched with advanced analytics to get the most out of the data.”

– Rainer Petke, Product Director at GfK, focusing on Advanced Analytics and gfknewron Predict

Discover how gfknewron Predict can unlock your competitive advantage

Look ahead: In our next article we shed light on how strong brands can keep prices more stable over time. Stay tuned!