.webp?width=832&height=592&name=customer-support%20(1).webp)

Car Finance (168)

Car Finance (168)

Cars & Gadgets (160)

Cars & Gadgets (160)

Car Maintenance (38)

Car Maintenance (38)

Tips & Advice (142)

Tips & Advice (142)

News (75)

News (75)

Road Trips (46)

Road Trips (46)

Pop Culture (188)

Pop Culture (188)

.webp?width=400&height=285&name=online-shoppers-with-dog%20(1).webp)

If you’re in the market for car finance, you’ll probably have heard about Hire Purchase – or HP for short – and leasing.

They’re two of the most popular types of finance and have more in common than you might think. Most importantly, they both let you spread the cost of a new or used car over several months or years and, in return, you’ll pay fixed monthly repayments plus interest.

But there are some key differences too.

So, which is better?

There’s no one-size-fits-all. When deciding whether HP or leasing is the right choice for you, it all depends on your individual circumstances, financial situation, and personal priorities.

Got a specific question? Why not jump to:

- How does hire purchase (HP) work?

- How does leasing work?

- What is the differences between the two options?

- What are the pros and cons of hire purchase?

- What are the pros and cons of leasing?

- What other alternatives are available?

- HP vs leasing: how do I decide which is right for me?

In a nutshell, what’s the difference between hire purchase and leasing?

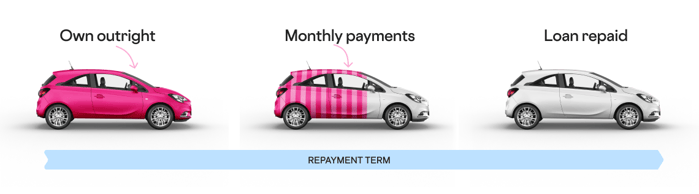

The big difference between HP finance and leasing is car ownership.

With HP, you’ll be working towards becoming your car’s legal owner. When you reach the end of your agreement, all your repayments are made, and you’ve paid the small Option to Purchase fee, it’ll be all yours!

Leasing rarely ends with you becoming the proud legal owner of a new set of wheels. While it can sometimes be an option if you’ve really fallen in love with the car during your lease, in most cases, you’ll simply hand the car back to the lender and walk away when the lease is up.

How does Hire Purchase work?

HP finance lets you spread the cost of a new or used car over a period of between one and six years (depending on the agreement length allowed by the lender).

You’ll usually need to put a deposit down upfront (although no deposit options are available) and then make fixed monthly repayments – plus interest – throughout the loan term.

The finance is secured against your vehicle, meaning you’ll be its registered keeper, but the lender will be its legal owner until your loan ends. Once you’ve made all your repayments and covered the transfer paperwork costs with the Option to Purchase fee, congratulations: you’re officially a car owner!

As its registered keeper, you’ll be responsible for the car’s upkeep, fuel, and insurance as soon as you sign your agreement, but you won’t be able to modify or sell it. Mileage restrictions also don’t usually apply with HP loans.

How does car leasing work?

Leasing – also known as Personal Contract Hire or PCH – is a lot like a long-term car rental.

Your lease will usually last between one and four years and you’ll pay a fixed monthly payment throughout. However, unlike HP, you won’t automatically become the car’s owner when your lease comes to an end.

If you’ve fallen hard for your leased vehicle and can’t bear the thought of letting it go, some lease companies will let you buy it at the end of your agreement. But there are no guarantees and most leases end with you handing the car back and walking away.

Like HP, you’ll probably have to put down a deposit upfront. The exact amount will depend on your agreement, but you might be asked to pay three, six, or even nine months’ worth of lease payments in advance.

Terms and conditions will apply. Most leases come with an annual mileage limit (and penalty charges if you go over it) and you’ll need to keep the car in good condition to avoid paying extra to cover the damage.

What are the differences between both options?

The big difference between HP and leasing is that one leads to car ownership and the other doesn’t, but that’s not the only thing that sets these types of finance apart:

Mileage restrictions

Leases usually come with an annual mileage limit, but with HP loans, you can drive as far as you like.

Fair wear and tear

As you’ll be handing the car back at the end of your lease, you’ll need to keep it in good condition. With HP, this only becomes an issue if you need to end your agreement early and give your car back to the lender.

Depreciation

HP finance normally leads to car ownership, which means any loss of value (depreciation) could affect the price you can sell it for in the future. With a lease, you don’t have to worry about this as you’re not the car owner.

More car finance guides

- What is Hire Purchase (HP) Finance?

- How Does Personal Contract Purchase (PCP) Car Finance Work?

- PCP vs Leasing: Which is Better?

What are the pros and cons of hire purchase?

There are a range of advantages and disadvantages of HP finance that you should think about before signing on the dotted line:

What are the pros and cons of leasing?

If you’re tempted by the thought of leasing a car instead of buying one with HP, here are a few advantages and disadvantages to help you make up your mind:

What other alternatives are available?

HP and leasing aren’t the only car finance options available. If these aren’t ticking the boxes for you because you’re looking for more flexibility, lower monthly repayments, or to be the car’s legal owner straightaway, you might want to consider these alternative types of car finance:

Personal Contract Purchase (PCP)

Personal Contract Purchase – or PCP – gives you options. Like HP, you’ll pay a deposit upfront and then make fixed monthly repayments for between one and five years. But PCP doesn’t have to lead to car ownership:

-

- When your PCP loan ends, you can make a large one-off payment to buy the car (known as the balloon payment), hand it back to the lender, or use any positive equity available as a deposit in a new deal.

- Instead of borrowing the car’s full purchase price, your loan payments will cover the difference between its current price and how much it’s estimated it’ll be worth at the end of your agreement (Guaranteed Minimum Future Value or GMFV).

- PCP can have lower monthly repayments than HP, but you’ll have to pay a large one-off balloon payment, usually equivalent to the GMFV, to become the car’s legal owner.

- An annual mileage limit will usually apply, and you’ll face an extra charge for every mile you go over it.

Personal loan

Personal loans are a different beast in the world of car finance as they (usually) aren’t secured against the vehicle. Instead, you’ll become the car’s legal owner as soon as you’ve used the loan to pay the dealer or private seller:

-

- As its legal owner, you’re free to sell the car, go on an epic road trip, add a giant spoiler, or install an ear-splitting sound system if you like. You just need to make sure you keep making loan repayments until the agreement ends.

- Unsecured loans present more of a risk to lenders, so they’re usually restricted to people with a solid payment history and good credit score.

- Monthly payments can be higher than other finance options.

HP vs leasing: how do I decide which is right for me?

There’s no right or wrong answer when choosing between HP and leasing. The best option for you will depend on your personal preferences, needs, and circumstances.