Based on the Modified PME method.

from pypme import verbose_xpme

from datetime import date

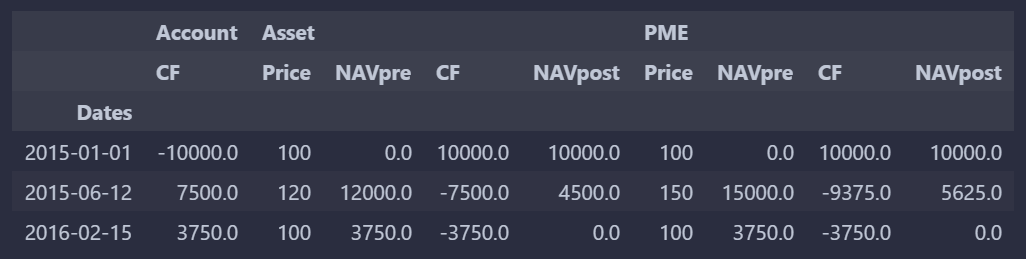

pmeirr, assetirr, df = verbose_xpme(

dates=[date(2015, 1, 1), date(2015, 6, 12), date(2016, 2, 15)],

cashflows=[-10000, 7500],

prices=[100, 120, 100],

pme_prices=[100, 150, 100],

)Will return 0.5525698793027238 and 0.19495150355969598 for the IRRs and produce this

dataframe:

Notes:

- The

cashflowsare interpreted from a transaction account that is used to buy from an asset at priceprices. - The corresponding prices for the PME are

pme_prices. - The

cashflowsis extended with one element representing the remaining value, that's why all the other lists (dates,prices,pme_prices) need to be exactly 1 element longer thancashflows.

xpme: Calculate PME for unevenly spaced / scheduled cashflows and return the PME IRR only. In this case, the IRR is always annual.verbose_xpme: Calculate PME for unevenly spaced / scheduled cashflows and return vebose information.pme: Calculate PME for evenly spaced cashflows and return the PME IRR only. In this case, the IRR is for the underlying period.verbose_pme: Calculate PME for evenly spaced cashflows and return vebose information.investpy_pmeandinvestpy_verbose_pme: Use price information from Investing.com. See below.

Use investpy_pme and investpy_verbose_pme to use a ticker from Investing.com and

compare with those prices. Like so:

from datetime import date

from pypme import investpy_pme

common_args = {

"dates": [date(2012, 1, 1), date(2013, 1, 1)],

"cashflows": [-100],

"prices": [1, 1],

}

print(investpy_pme(pme_ticker="Global X Lithium", pme_type="etf", **common_args))

print(investpy_pme(pme_ticker="bitcoin", pme_type="crypto", **common_args))

print(investpy_pme(pme_ticker="SRENH", pme_type="stock", pme_country="switzerland", **common_args))Produces:

-0.02834024870462727

1.5031336254547634

0.3402634808264912

The investpy functions take the following parameters:

pme_type: One ofstock,etf,fund,crypto,bond,index,certificate. Defaults tostock.pme_ticker: The ticker symbol/name.pme_country: The ticker's country of residence. Defaults tounited states.

Check out the Investpy project for more details.

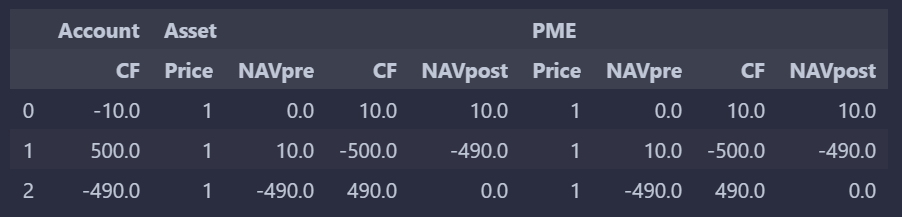

Note that the library will only perform essential sanity checks and otherwise just works with what it gets, also with nonsensical data. E.g.:

from pypme import verbose_pme

pmeirr, assetirr, df = verbose_pme(

cashflows=[-10, 500], prices=[1, 1, 1], pme_prices=[1, 1, 1]

)Results in this df and IRRs of 0: